SAICA Welcomes Treasury Changes To Budget Process

Johannesburg, 31 July 2025 – The South African Institute of Chartered Accountants (SAICA) welcomes positive changes announced by National Treasury on 23 July 2025 that should assist the country in creating a budget and budget process that is not only efficient, but also effective in dealing with the needs of South Africa, its people and the unique challenges and trade-offs we face.

National Treasury announced that it will be changing the medium-term budget process for 2025, this in relation to the 2025/2026 fiscal year that we are currently in. This change is spurred by a desire to align to the country’s changing realities, incorporating the learnings from Budget 2025 and inputs considered in this regard. The key changes to be actioned are outlined in the 2026 MTEF guidelines. It is expected that similar changes will apply to Budget 2026 for the 2026/2027 fiscal year.

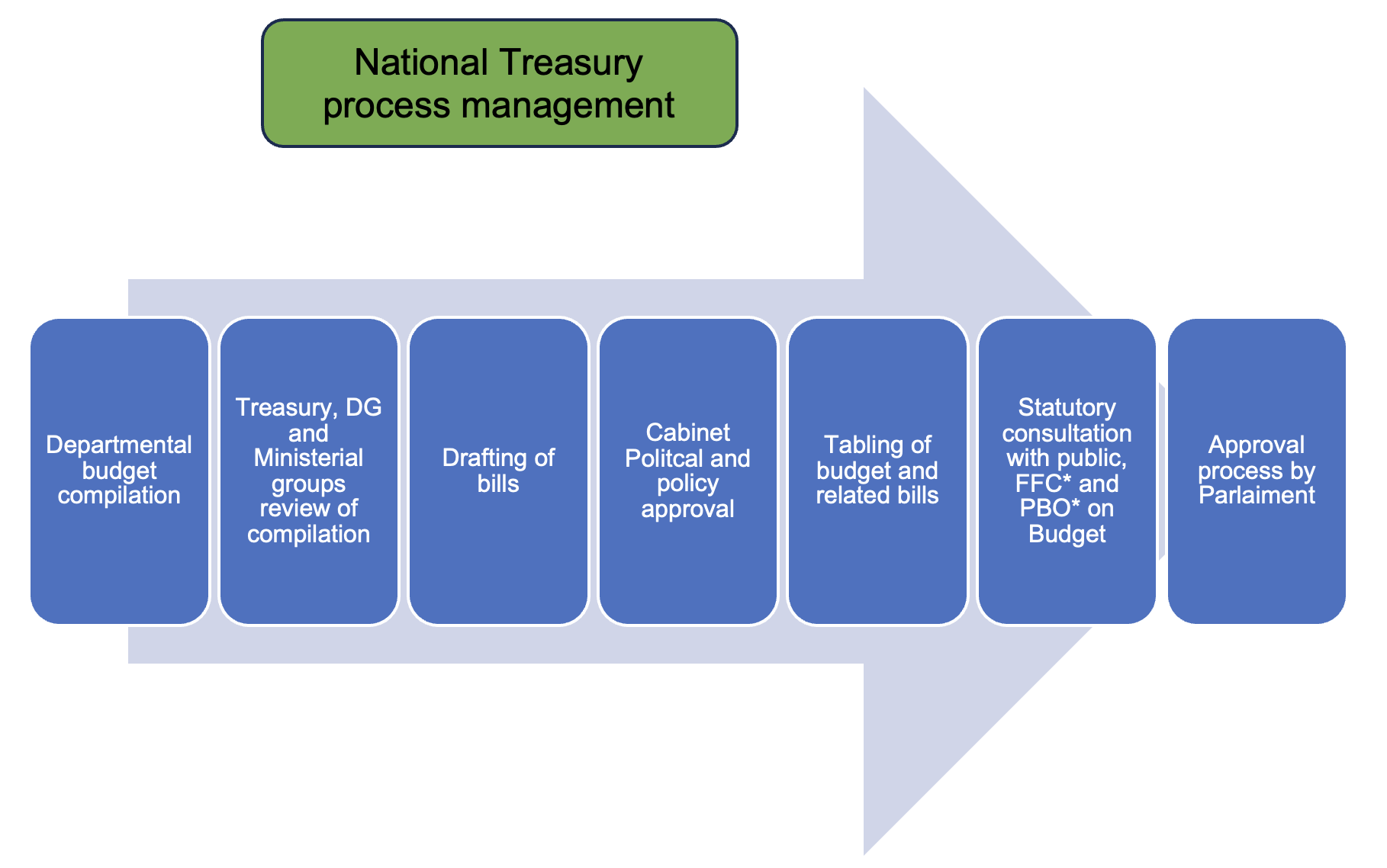

Conceptually the budget process historically could be summarised as follows:

*FFC is the Financial and Fiscal Commission and PBO is the Parliamentary Budget Office

However, Pieter Faber, Head of Taxation at SAICA, indicates that due to the change in the country’s political landscape coupled with the fiscal realities, Budget 2025 more than previous years, revealed challenges with this process and the misalignments it creates. “This process creates the incorrect impression that National Treasury and the Minister of Finance were the sole custodians of the budget and were in fact solely responsible for its success or failure. In reality National Treasury is merely the custodian of the compilation process, Parliament remains the ultimate approver and carries responsibility for the Budget it approves, including ensuring that it aligns to the constitutional prescripts”, explained Faber. He further went on to clarify that the timing of how the Budget compilation process was managed, including step approvals, created further challenges. “This review does not, however, address that Parliament is left with little time to review, consult on and approve the Budget”.

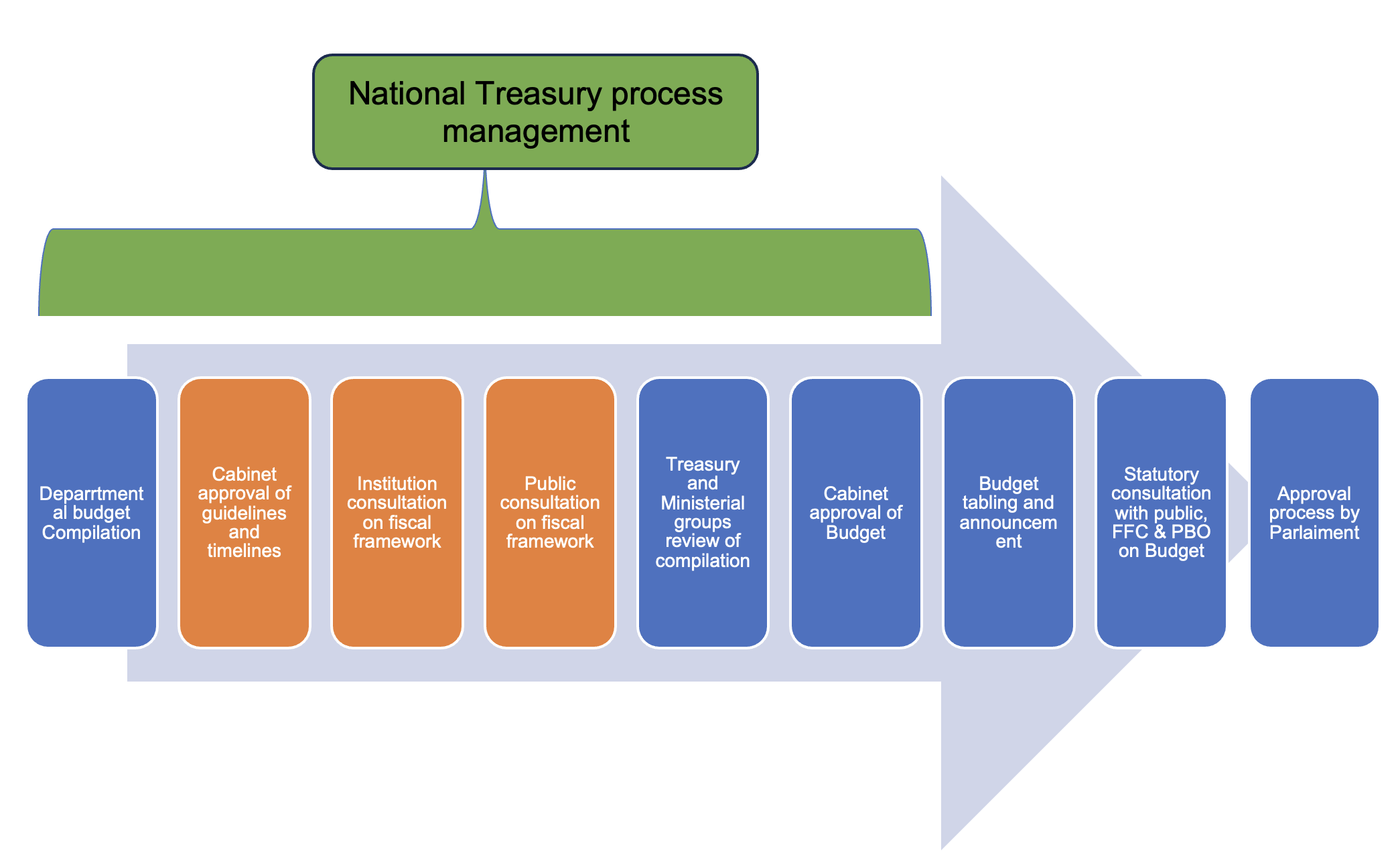

The new budget process takes a more consultative approach and also seeks to get “approvals” at key junctures of the process to avoid and minimise misalignment by key persons later in the process. The new process can be summarised as follows:

SAICA welcomes the above changes that will ensure that Treasury have the relevant buy-in before the Budget process unfolds too far down the road, allowing for course corrections where required without delaying the process. “It is our hope that steps like consulting with institutions will include the National Economic Development and Labour Council (NEDLAC), FFC and other legally compelled consultation parties, as well as the PBO. The latter, as the advisor to Parliament, as ultimate approver of the budget, ensures that Parliament also has earlier insights into the policy direction and that core concerns can be addressed before the Budget is tabled, ensuring that the Budget is not a surprise to them – affording them, the opportunity to properly apply their minds to complex facts in a complex environment”, states Faber.

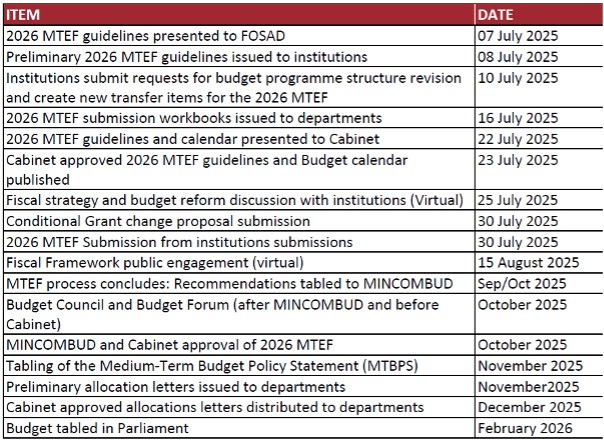

The timelines for the 2026 Medium-term Expenditure Framework (MTEF) as it relates to the process is highlighted below, having been publicly published after Cabinet approved it on 23 July 2025. It is anticipated that a similar calendar and plan will be applied to Budget 2026.

As part of the public engagement on 15 August 2025 on the fiscal framework, it may be prudent to also understand the process, or at which step the fiscal framework is aligned to the economic policy, which is currently the National Development Plan 2030 as the fiscal framework is merely the execution strategy on this. Additionally it would also be insightful to understand how the timelines cater for when a specific step is not approved and the previous step(s) have to be redone or altered; as in the case of Budget 2025.

It is however not the budget speech and documents that enable fiscal obligation, as that is rather the broader execution plan underpinned by numerical data and principles. It is instead the “budget legislation” that embodies and effects the budget as approved by Parliament and enacted by the President. “In this regard there are two sets of legislation, namely those issued with the budget and those issued afterwards. The first set includes the Appropriation Bill that determines what money is to be spent by the various National Government departments and entities, as well as how much each receives. The first batch also includes the Division of Revenue Bill that divides the budget between National, Provincial and Local government. Lastly, of the first batch, is the Rates and Monetary Amounts Bill which determines the tax rates that will be applied to taxpayers for the coming tax year. The second set of bills are the Taxation Laws and Tax Administration bills which determine the scope of specific taxing provisions or tax allowances/deductions and also regulate SARS’ and taxpayers’ rights and obligations”, Faber articulates.

Both these sets of bills are approved in terms of processes adopted by Parliament, who as the constitutional representatives of the people of South Africa, seek to “quality control” the proposals made by government whilst also measuring the proposals against the relevant constitutional requirements for responsible spending, debt, economic growth and fair and efficient tax administration. However as South Africa is a participative democracy, where the people form part of the legislative process, Parliament is compelled to also consult with them and it has both a model and framework for this. Some of these processes are time sensitive with public comment on the budget usually due in 3 business days and on the second set of legislation usually 2-3 weeks; and these may require similar review to the Budget process.

SAICA looks forward to the new consultative budget process managed by National Treasury and also to participating in it. Similarly, we hope that any learnings can, where applicable, be transferred to the Parliamentary legislative process to ensure a similar enhanced consultation and consensus process that delivers on a better outcome and life for all South Africa’s people.

Issued by the SAICA Corporate Affairs Team

About SAICA

The South African Institute of Chartered Accountants (SAICA), South Africa’s pre-eminent accountancy body, is recognised as the world’s leading accounting institute and is home to the leading CA designation in the world The Institute provides a wide range of support services to more than 60 000 members and associates who are chartered accountants (CAs[SA]), as well as associate general accountants (AGAs[SA]) and accounting technicians (ATs[SA]), who hold positions as CEOs, MDs, board directors, business owners, chief financial officers, auditors and leaders in every sphere of commerce and industry, and who play a significant role in the nation’s highly dynamic business sector and economic development.

SAICA is a member of Chartered Accountants Worldwide (CAW), a global family that connects over 1,8 million fellow Chartered Accountants and students in more than 190 countries. Together, we support, develop, and promote the role of Chartered Accountants as trusted business leaders, difference makers, and advisers.

SAICA Media Contact

Kgauhelo Dioka,

***@saica.co.za

Manager: Public and media relations

Acting Lead: Corporate Affairs

SAICA Customer Experience Division